benkey

Member

- First Name

- Ben

- Joined

- Jun 2, 2021

- Threads

- 1

- Messages

- 5

- Reaction score

- 2

- Location

- Savannah, GA

- Vehicle(s)

- Mazda CX-9

- Occupation

- Engineer

- Thread starter

- #1

Have decided to join the Jeep family with Gladiator. Deciding between lease vs buy.

Here are the numbers for lease I got.

Trim Sport S Diesel engine

Msrp: $50,115

Residual value: $36,500

Term: 36 months

Down payment; $2,000

Monthly payment: $700

if I do the numbers, I pay $27,200 for driving the Jeep for 3 years that depreciates by only $13,615. Of course the tax and paperwork adds about $1,800. I live in GA.

I think the lease numbers are absurd. Better off to buy the Jeep.

Has anybody recently leased their Jeep? If so, would you share your numbers so that I can know how much I am off?

thanks

Here are the numbers for lease I got.

Trim Sport S Diesel engine

Msrp: $50,115

Residual value: $36,500

Term: 36 months

Down payment; $2,000

Monthly payment: $700

if I do the numbers, I pay $27,200 for driving the Jeep for 3 years that depreciates by only $13,615. Of course the tax and paperwork adds about $1,800. I live in GA.

I think the lease numbers are absurd. Better off to buy the Jeep.

Has anybody recently leased their Jeep? If so, would you share your numbers so that I can know how much I am off?

thanks

Sponsored

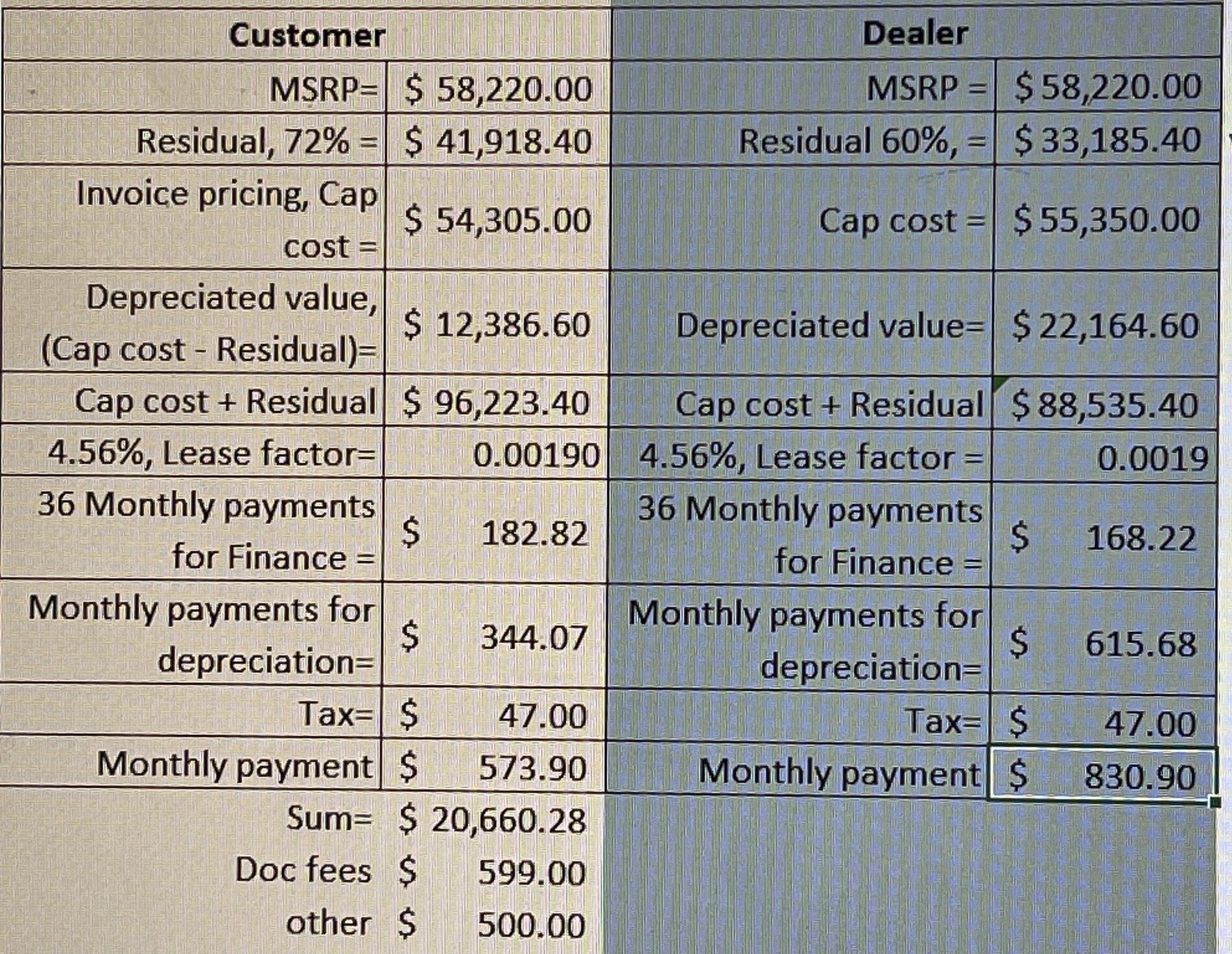

") ). numbers on my Overland lease:

). numbers on my Overland lease: