Sponsored

It seems it's not just Jeeps that have poor value vs. their loans.

Jefe1018

Well-Known Member

How could anyone possibly imagine that a car note of $20,000 over MSRP on a vehicle you are 100% financing would put you upside down?

Flyboy2109

Well-Known Member

- First Name

- Fred

- Joined

- Dec 17, 2022

- Threads

- 6

- Messages

- 281

- Reaction score

- 373

- Location

- Washington

- Vehicle(s)

- 2023 Gladiator, 2004 CTS-V, 2001 Tahoe, 1990 Dakot

- Occupation

- retired Pilot: USCG, Delta, Netjets

Of course one is upside down on a car loan! It is what was always referred to as "Taillight Depreciation'. As soon as the brake lights flash off the dealer lot the vehicle is now 'used" and worth much less on the market as it's now a one owner car to a second buyer.

Wheelin98TJ

Well-Known Member

- First Name

- Ryan

- Joined

- Jul 27, 2021

- Threads

- 12

- Messages

- 3,732

- Reaction score

- 4,392

- Location

- Devils Lake, MI

- Vehicle(s)

- 2021 Jeep Gladiator

- Occupation

- Bean Counter

Usually this is true, but there are rare exceptions. I have an F150 with a 0% loan that I haven't been upside down on since I bought it August 2020. But that's due to the market going nuts after I bought it and of course the 0% loan.Of course one is upside down on a car loan! It is what was always referred to as "Taillight Depreciation'. As soon as the brake lights flash off the dealer lot the vehicle is now 'used" and worth much less on the market as it's now a one owner car to a second buyer.

Janster

Well-Known Member

- First Name

- Jandy

- Joined

- Mar 27, 2024

- Threads

- 42

- Messages

- 1,914

- Reaction score

- 2,961

- Location

- Lancaster, PA

- Vehicle(s)

- 2024 Gladiator Mojave X

- Occupation

- Biller

I’m not surprised…… A LOT of people are un-informed and mis-informed about financials and/or they don’t care. “I’m in debt up to my eyeballs”

I’ve known at least 2 people in my lifetime who went thru bankruptcy - TWICE!! Taking the easy way out….cuz after the bankruptcy, they were able to open up new credit cards and continue spending foolishly. Why bother paying your bills when you CAN have your cake and eat it to.

I’ve known at least 2 people in my lifetime who went thru bankruptcy - TWICE!! Taking the easy way out….cuz after the bankruptcy, they were able to open up new credit cards and continue spending foolishly. Why bother paying your bills when you CAN have your cake and eat it to.

Sponsored

DailyMoparGuy

Well-Known Member

I expect that number to get worse given how stupid high car prices are right now. Imagine someone financing $60k for one of those shitty Toyota Trailhunters today….maybe it’ll hold its value like the old TRD Pros but idk lately.

Edit: Sixty f**king thousand dollars for a Tacoma! It is mind blowing to me that people are paying that for it. A couple thousand away from a Ram 2500 with the Power Wagon package. Different tool, I know, but goodness.

Edit: Sixty f**king thousand dollars for a Tacoma! It is mind blowing to me that people are paying that for it. A couple thousand away from a Ram 2500 with the Power Wagon package. Different tool, I know, but goodness.

Janster

Well-Known Member

- First Name

- Jandy

- Joined

- Mar 27, 2024

- Threads

- 42

- Messages

- 1,914

- Reaction score

- 2,961

- Location

- Lancaster, PA

- Vehicle(s)

- 2024 Gladiator Mojave X

- Occupation

- Biller

New Gladiators are $70K….. Welcome to the new norm of our economy. If you haven’t noticed, EVERYTHING is more expensive. None of that is gonna change….‘Edit: Sixty f**king thousand dollars for a Tacoma! It is mind blowing to me that people are paying that for it. A couple thousand away from a Ram 2500 with the Power Wagon package. Different tool, I know, but goodness.

I will say…. Back when I was shopping in 2016… Loaded GMC CAnyon was $40K. The TAcoma was about the same but was EXTREMELY lacking in options & features. They didn’t even have power seats or rear disc brakes.

I would tend to believe … The Tacoma is still lacking in features & available options compared to the Gladiator.

Bbannongmu

Well-Known Member

Vehicles are almost always depreciating assets. Pre Covid (aka Plandemic) seems to make a big difference. I have about $2,800 left on my loan and my 2020 JTR is worth about $30k. Bought it for about $47k plus tax, tags . Got about $14k for my paid off 2013 JKU as a trade in and 2% financing. $17k depreciation in 56 months or about $300 a month average, seems reasonable. I’ll probably keep it another 5 years or more as my DD and if it doesn’t cost me a fortune to keep on the road and it’s still worth anything then, I’ll be happy with my decision.

Riverdog

Well-Known Member

- Joined

- Aug 26, 2024

- Threads

- 3

- Messages

- 115

- Reaction score

- 211

- Location

- Upstate NY

- Vehicle(s)

- 2020 Jeep Gladiator Sport

- Occupation

- Software Engineer

Jeeps traditionally hold their value better than most vehicles. The Gladiators have been over priced from the start. I wanted a new Mojave when they came out, the cost was insane. Instead bought a Sierra AT4 with a 6.2L and 420 hp for $56k. I had put 20k down on that truck in 2021 and 3 years later I traded it in on my used 2020 JT sport and walked out debt free. This sport is 1/2 the truck the AT4 was but I'm happy enough considering it's paid for.

KX L

Well-Known Member

- First Name

- KX

- Joined

- May 1, 2019

- Threads

- 21

- Messages

- 578

- Reaction score

- 788

- Location

- Lake St Louis MO

- Vehicle(s)

- 2017 CVO Street Glide; 2022 JT Mojave with 6MT

- Occupation

- Retired

Great points by all. My 22 Mojave stickered at $68,7xx as I ordered every option except the smoker group. Including the half doors. Because of this forum I bought through TriCity motors in NC and got 5% off. But I knew I was going to pay out the nose as I intend for it to be my forever truck. Most importantly because I have great credit I got the loan for 1.99% from USAA. That's the bottomline. Everything below is just a story I have about debt so don't waste your time if you have things to do.

With my wife and friend.

I had a friend in class with me at Motorcycle Mechanics Institute in Phoenix in 2017 and 18. I'm a retired USMC Colonel with over 30 years of active duty service and he's a retired Air Force Master Sergeant with 28 years of active duty service. He was twice divorced and literally had a brand new Harley and then a big new Ford truck with all the options. We were both getting school and some living expenses paid for by the GI Bill [Thanks very very much to all of you that are paying United States taxes.]

When he bought the truck a couple of months after the Bike I asked him how he could afford it? He said, "The payments fit into my budget."

Needless to say, I had him over for dinner and we went through his budget----and what he thought he "owned". He was shocked to find out he was $350,000 in debt and overpaying hugely for each item due to interest on each of the things he'd bought---at horrible interest rates because he didn't have even good credit. I explained to him that living in debt is living in the past and making minimum payments on many items is akin to putting a financial bullet to your own head and pulling the trigger.

He was a really smart guy [honor grad of our class] but ignorant as no one had ever really explained how money works. I explained rule one is to always pay yourself first. First to have a couple of months worth of expenses in a savings account. Then to pay off the highest interest rate loans [NOT THE SMALLEST Loan]. Daily decisions have to be made on whether it be in paying off debt early or buying that Starbucks twice a day. I told him DON'T stop having pocket change to buy daily things you want to have a great life and you've earned it. But also DON'T ever take out another loan until all your current ones are paid off.

For him it was an instant life style change and with his rock hard self discipline he completely changed literally overnight. Got rid of the new truck for a 4 year old used one [with few bells and whistles] and walked out of the dealer owing less than $500. He went from buying rounds all the time for everyone to ensuring everyone else bought rounds also when we all went out. In short he stopped thinking about what was in his pocket to spend to instead what he could do to benefit himself first with the money he had earned.

This why I saved for 2 years before ordering my truck at a 5% discount from TriCity Jeep and also why I'm still paying a bit more than the minimum payment each month [decreases how much I ultimately pay in interest].

My loan could easily be paid off but at the rate of 1.99%, for me [the wife likes to travel] it makes sense to keep paying that percent of 2022 dollars in order to have prepaid for our vacations---this year we're heading to Hawaii for the month of December [3 Dec-5 Jan] and it's fully paid for [housing, rental jeep, and living expenses] in one of my savings accounts.

Probably every one of you has read about the old lady teacher or school janitor who died with over a million dollars to donate to a worthy cause. It can be done on a very small salary.

My dad and mom had 8 kids in 13 years [stupid Catholic religion]---after the 8th he just tied her tubes]---everything I got was a hand me down but he taught us all about money and the need to tithe and pay yourself first. Every month he announced how much he saved. There were many months throughout the early 60's of him telling us he was able to put a nickle[!] [he always made it sound exciting] in savings that month. Even as young kids we scoffed at that. But he kept talking about habits and how money compounds and grows. After paying off his medical school loans he was able to tell us monthly about hundreds and then thousands in savings.

Each kid had a bank account with him. He paid us the going interest rate. He also charged the going interest rate when we borrowed more than we had. I was very sad to lose him to cancer when he was only 53 and I was 23.

With my wife and friend.

I had a friend in class with me at Motorcycle Mechanics Institute in Phoenix in 2017 and 18. I'm a retired USMC Colonel with over 30 years of active duty service and he's a retired Air Force Master Sergeant with 28 years of active duty service. He was twice divorced and literally had a brand new Harley and then a big new Ford truck with all the options. We were both getting school and some living expenses paid for by the GI Bill [Thanks very very much to all of you that are paying United States taxes.]

When he bought the truck a couple of months after the Bike I asked him how he could afford it? He said, "The payments fit into my budget."

Needless to say, I had him over for dinner and we went through his budget----and what he thought he "owned". He was shocked to find out he was $350,000 in debt and overpaying hugely for each item due to interest on each of the things he'd bought---at horrible interest rates because he didn't have even good credit. I explained to him that living in debt is living in the past and making minimum payments on many items is akin to putting a financial bullet to your own head and pulling the trigger.

He was a really smart guy [honor grad of our class] but ignorant as no one had ever really explained how money works. I explained rule one is to always pay yourself first. First to have a couple of months worth of expenses in a savings account. Then to pay off the highest interest rate loans [NOT THE SMALLEST Loan]. Daily decisions have to be made on whether it be in paying off debt early or buying that Starbucks twice a day. I told him DON'T stop having pocket change to buy daily things you want to have a great life and you've earned it. But also DON'T ever take out another loan until all your current ones are paid off.

For him it was an instant life style change and with his rock hard self discipline he completely changed literally overnight. Got rid of the new truck for a 4 year old used one [with few bells and whistles] and walked out of the dealer owing less than $500. He went from buying rounds all the time for everyone to ensuring everyone else bought rounds also when we all went out. In short he stopped thinking about what was in his pocket to spend to instead what he could do to benefit himself first with the money he had earned.

This why I saved for 2 years before ordering my truck at a 5% discount from TriCity Jeep and also why I'm still paying a bit more than the minimum payment each month [decreases how much I ultimately pay in interest].

My loan could easily be paid off but at the rate of 1.99%, for me [the wife likes to travel] it makes sense to keep paying that percent of 2022 dollars in order to have prepaid for our vacations---this year we're heading to Hawaii for the month of December [3 Dec-5 Jan] and it's fully paid for [housing, rental jeep, and living expenses] in one of my savings accounts.

Probably every one of you has read about the old lady teacher or school janitor who died with over a million dollars to donate to a worthy cause. It can be done on a very small salary.

My dad and mom had 8 kids in 13 years [stupid Catholic religion]---after the 8th he just tied her tubes]---everything I got was a hand me down but he taught us all about money and the need to tithe and pay yourself first. Every month he announced how much he saved. There were many months throughout the early 60's of him telling us he was able to put a nickle[!] [he always made it sound exciting] in savings that month. Even as young kids we scoffed at that. But he kept talking about habits and how money compounds and grows. After paying off his medical school loans he was able to tell us monthly about hundreds and then thousands in savings.

Each kid had a bank account with him. He paid us the going interest rate. He also charged the going interest rate when we borrowed more than we had. I was very sad to lose him to cancer when he was only 53 and I was 23.

Sponsored

NVjeff

Well-Known Member

- First Name

- Jeff

- Joined

- Dec 17, 2023

- Threads

- 5

- Messages

- 168

- Reaction score

- 245

- Location

- Carson Valley

- Vehicle(s)

- 2023 JT

- Occupation

- Retired

Congrats Col. and thanks for explaining things to your friend.

It's not hard yet so many smart people get in trouble with money.

I've been following this thread and thinking about things.

Every vehicle I've bought I put enough down that I'm not upside down on it.

This gives me the option to sell it if I find I can't afford the payment due to unforeseen changes in my financial situation.

I may have to give it away due to the outstanding loan amount, but I'll be out from under it and my credit rating will remain intact.

Banks, credit card company's, auto manufacturers, any money lenders are after one thing.

To get people in harness (in debt to them) making payments on excessive interest rates. This allows them to not work as hard, take it easy, maybe retire early.

Meanwhile the people that owe them money continue to work, making payments and probably taking out more loans to cover common expenses.

Then when the economy turns to shit these people don't have any reserves, either in the bank or in their budget, to cover the rising costs.

It's not hard yet so many smart people get in trouble with money.

I've been following this thread and thinking about things.

Every vehicle I've bought I put enough down that I'm not upside down on it.

This gives me the option to sell it if I find I can't afford the payment due to unforeseen changes in my financial situation.

I may have to give it away due to the outstanding loan amount, but I'll be out from under it and my credit rating will remain intact.

Banks, credit card company's, auto manufacturers, any money lenders are after one thing.

To get people in harness (in debt to them) making payments on excessive interest rates. This allows them to not work as hard, take it easy, maybe retire early.

Meanwhile the people that owe them money continue to work, making payments and probably taking out more loans to cover common expenses.

Then when the economy turns to shit these people don't have any reserves, either in the bank or in their budget, to cover the rising costs.

Alan_Hepburn

Well-Known Member

- First Name

- Alan

- Joined

- May 8, 2020

- Threads

- 23

- Messages

- 302

- Reaction score

- 322

- Location

- Lewisburg, TN USA

- Vehicle(s)

- 2020 JT Sport S; 2022 JLU Spport S; 2007 Fleetwood Bounder 35E

- Occupation

- Retired

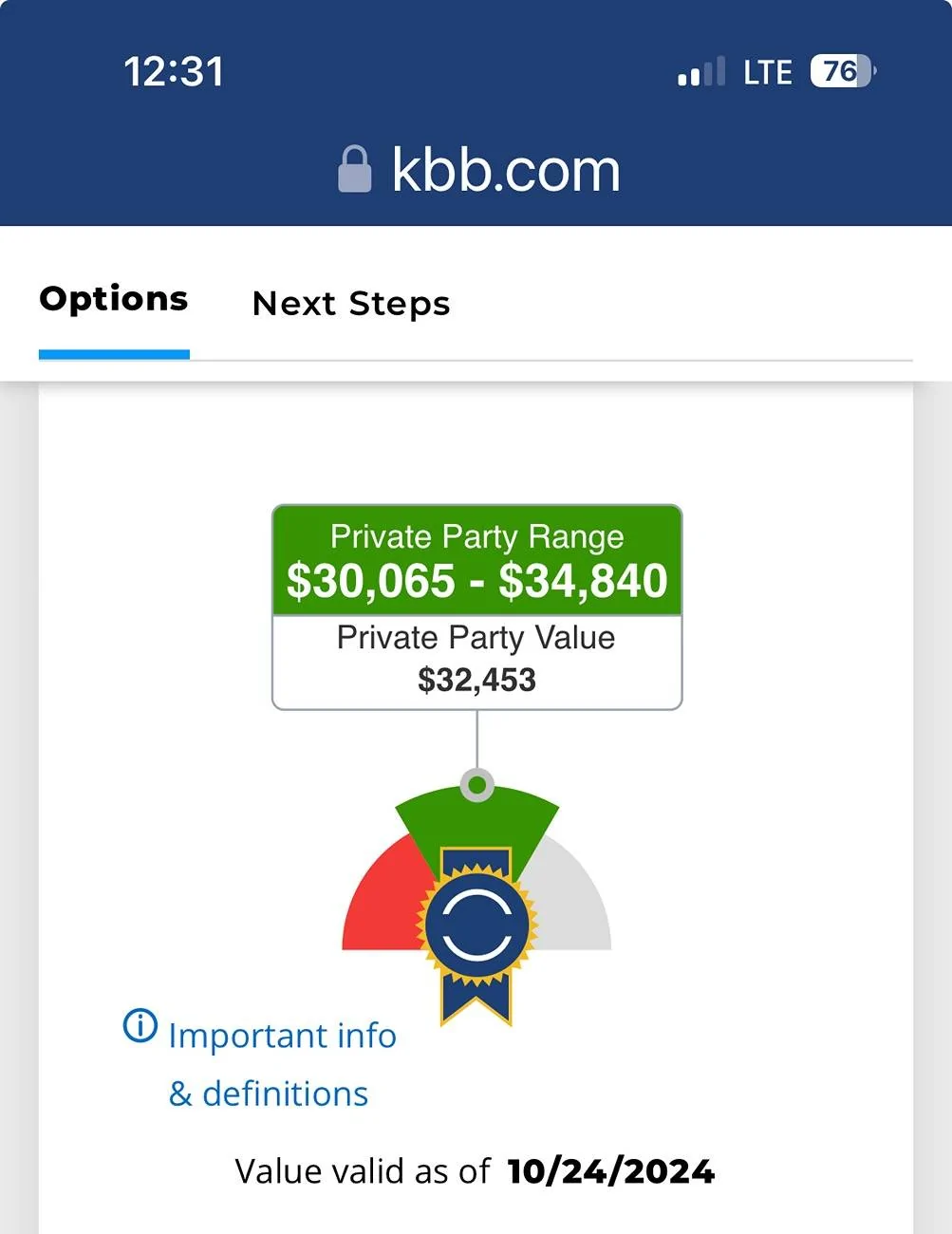

We hit the market at the exact RIGHT time: in 2019 we paid about $24K for a 2017 JKU Sport S. In 2021 Vroom offered us $32K for it - we jumped on that offer and used the proceeds to order a 2022 JLU SS!

Sponsored

Similar threads

- Replies

- 5

- Views

- 1,443

- Replies

- 12

- Views

- 2,591